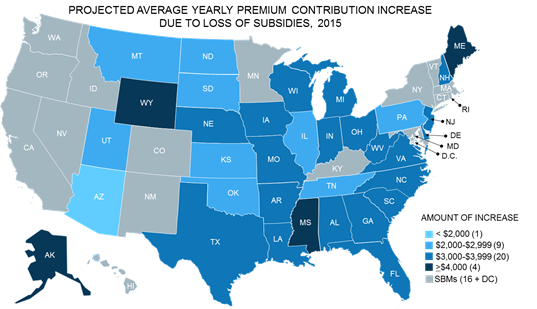

Consumers could face average annual premium contribution increases of $3,300 in 2015, if the Supreme Court rules tax credits are illegal in states with a federal exchange, according to new analysis from Avalere.[1] The Supreme Court is expected to rule imminently on whether 6.4 million Americans can continue to receive tax credit subsidies through federal exchanges in 34 states. Florida and Texas would have the most number of state residents impacted by the ruling—1.3 million and 0.8 million respectively (see Table 1).

“Exchange enrollees are currently subsidized at a very high rate,” said Elizabeth Carpenter, director at Avalere. “As a result, many individuals would likely find exchange premiums unaffordable without the tax credits provided under the law. If the Court rules for King, many current enrollees are expected to drop coverage.

In 2015, 85 percent of enrollees in federal exchange states receive a tax credit subsidy. On average, these enrollees are subsidized at a rate of $3,300 for the year. However, subsidies vary by income and the premiums in a given geography. As a result, premium contribution increases stemming from the Supreme Court ruling would vary by state, ranging from $6,400 average in Alaska, to a $1,900 in Arizona (see Table 1). These estimates reflect only the loss of subsidies in 2015 based on current premiums in the market.[2] If the Supreme Court ruling results in many exchange enrollees dropping coverage, it could materially impact the risk-pool in both 2015 and future years.[3] Some states have already permitted exchange plans to file two sets of rates for 2016, contingent on the Supreme Court ruling, while others have indicated that plans may be able to refile following the verdict.[4]

“We can’t assume that consumers will simply be able to return to previous sources of coverage if subsidies are struck down,” said Dan Mendelson, CEO at Avalere. “The ACA has fundamentally shifted the insurance market, and the elimination of subsidies would mean the vast majority of those adversely affected will struggle to maintain access to care.”

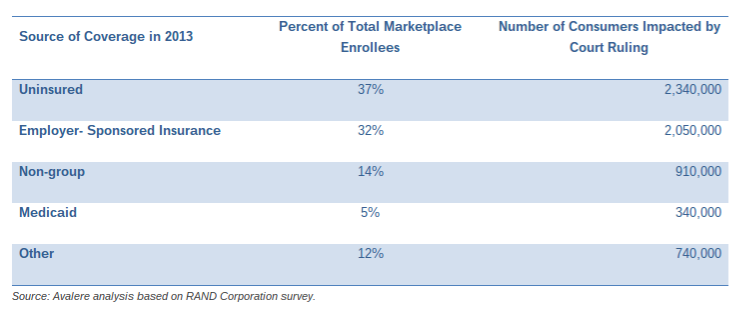

Indeed, many exchange consumers will not only find it difficult to continue to afford insurance without subsidies, others will likely be unable to return to their previous source of coverage. A recent survey by the Rand Corporation estimated the previous source of coverage for exchange enrollees as of February 2015.[5]

After applying these findings to the population potentially impacted by the Supreme Court ruling, Avalere estimates approximately 2.3 million exchange enrollees – 37 percent of those enrolled – were likely to be uninsured before enrolling in exchange coverage. These consumers are unlikely to continue purchasing coverage without subsidies.

Another 32 percent of those affected by the ruling—about 2 million enrollees—transitioned to marketplace coverage from employer-sponsored insurance. While some of these employees may be able to rejoin their employer-sponsored insurance plan, reports from insurance companies indicate that many small employers may have stopped offering coverage after exchanges launched in 2014.

Finally, 14 percent or almost 1 million exchange enrollees joined the market from non-group insurance offered prior to the establishment of exchanges. While this market is still in place, the introduction of insurance market reforms, essential health benefits, and patient protections mean that much of the coverage these individuals previously purchased may be unavailable or available at increased cost.

“If the Court rules against the subsidies, Congress, the Administration, and the states will face immense pressure to take action,” said Caroline Pearson, senior vice president at Avalere. “While some stakeholders may advocate for a short-term fix, others may see the ruling as an opportunity to reform the Affordable Care Act more broadly.”

Methodology

Analysis assumes consumers do not switch plans following the ruling and that 2015 plan premiums remain at current levels. Loss of subsidies will be considered a qualifying event for a special enrollment period, and therefore consumers would have the option to select a less-expensive plan. However, carriers in the FFE may be permitted to terminate contracts with the exchange under certain scenarios, which could reduce coverage offerings.

While Nevada, New Mexico, and Oregon all rely on HealthCare.gov infrastructure in 2015, Avalere considers them state-based exchanges for the purposes of this analysis.

Using the RAND study, Avalere applies the RAND study to the subsidy eligible population to determine previous source of insurance. For the purpose of this analysis, Avalere assumes that the whole market distribution studied by RAND is similar to the distribution of subsidized enrollees.

Premium increases and the number of individuals who will be impacted by the ruling are based on “March 31, 2015 Effectuated Enrollment Snapshot,” Centers for Medicare & Medicaid Services, June 2, 2015.

TABLE 1: Average Premium Contribution Increase and Individuals Affected, by State, 2015

States Average Yearly Premium Contribution Increase Number of People Affected

FFE $3,300 6,388,000

AK $6,400 17,000

AL $3,200 132,000

AR $3,400 48,000

AZ $1,900 127,000

DE $3,200 19,000

FL $3,500 1,325,000

GA $3,300 412,000

IA $3,200 34,000

IL $2,500 232,000

IN $3,800 160,000

KS $2,500 70,000

LA $3,900 138,000

ME $4,000 61,000

MI $3,300 228,000

MO $3,300 198,000

MS $4,200 76,000

MT $2,800 42,000

NC $3,800 459,000

ND $2,800 14,000

NE $3,100 57,000

NH $3,200 30,000

NJ $3,800 172,000

OH $3,100 161,000

OK $2,500 87,000

PA $2,700 349,000

SC $3,400 154,000

SD $2,700 17,000

TN $2,600 156,000

TX $3,000 832,000

UT $2,500 86,000

VA $3,100 286,000

WI $3,800 166,000

WV $3,800 26,000

WY $5,100 17,000

FFE: Federally Facilitated Exchange

[1] Avalere analysis of the Centers for Medicare & Medicaid Services (CMS) “March 31, 2015 Effectuated Enrollment Snapshot”. Released June 2, 2015. http://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2015-Fact-sheets-items/2015-06-02.html.

[2] Under current insurance rules, it is unlikely that plans will be permitted to refile rates in 2015. As such, we do not assume any changes in the unsubsidized plan premiums for 2015.

[3] American Academy of Actuaries, Letter to Secretary Burwell, February 24, 2105. http://d35brb9zkkbdsd.cloudfront.net/wp-content/uploads/2015/02/Actuary-Letter.pdf

[4] Alaska, Indiana, Nebraska, North Dakota, and Texas all stated that they would accept two sets of rates for 2016. Other states, including Florida’s Department of Insurance, indicated that they may allow issuers to refile rates if the Supreme Court rules against the administration

[5] Katherine G. Carman, Christine Eibner and Susan M. Paddock. Trends In Health Insurance Enrollment, 2013-15. Health Affairs, no. (2015): doi: 10.1377/hlthaff.2015.0266.

Avalere Health is a strategic advisory company whose core purpose is to create innovative solutions to complex healthcare problems. Based in Washington, D.C., the firm delivers actionable insights, business intelligence tools and custom analytics for leaders in healthcare business and policy. Avalere's experts span 230 staff drawn from Fortune 500 healthcare companies, the federal government (e.g., CMS, OMB, CBO and the Congress), top consultancies and nonprofits. The firm offers deep substance on the full range of healthcare business issues affecting the Fortune 500 healthcare companies. Avalere’s focus on strategy is supported by a rigorous, in-house analytic research group that uses public and private data to generate quantitative insight. Through events, publications and interactive programs, Avalere insights are accessible to a broad range of customers. For more information, visit avalere.com, or follow us on Twitter @avalerehealth.